Weekly Highlights - July 9, 2022

Recent developments for Kohl's, Spirit Airlines, and Magnachip

Kohl’s (KSS)

Bad news first. On July 1, 2022, Kohl’s (which I highlighted as an event-driven idea on May 20) announced the conclusion of its strategic process and the board’s decision to stop pursuing an acquisition by Franchise Group (FRG).

FRG submitted a $60 bid in early June and was offered a 3-week exclusive engagement period, but ultimately reduced its bid to $53 given an increasingly challenging financing and retail environment. My guess is that they could not obtain the remaining financing and simply had to go with a lower bid. Obviously, shares dropped following the announcement, from $36 to $29.

As part of the press release, Kohl’s also provided Q2 guidance reflecting this challenging retail environment and is now expecting sales to be down high-single digits, compared to prior expectations of low-single digits. However, the company reaffirmed its commitment to executing a $500 million Accelerated Share Repurchase program (> 10% of its market capitalization), to commence immediately after Q2 earnings. In addition, the company announced its plan to evaluate the monetization of part of its real estate portfolio.

So where do we go from here? It is never a good sign when a special situation turns into a long-term holding, but in the case of Kohl’s I believe it makes sense and I think the board made the right decision to reject FRG’s lowball offer:

While the narrative has been that retail and department stores are dying, Kohl’s revenues and EBITDA have been very resilient over the past 20 years outside of the Covid period, even including the Global Financial Crisis:

Its balance sheet is solid, with $8 billion of real estate assets and less than $2 billion of long-term debt (excluding operating leases liabilities). Since FRG bid was largely financed through a sale-leaseback transaction with Oak Street, we can be relatively confident that the property portfolio has value and Kohl’s has announced that it is taking steps to monetize portion of these assets.

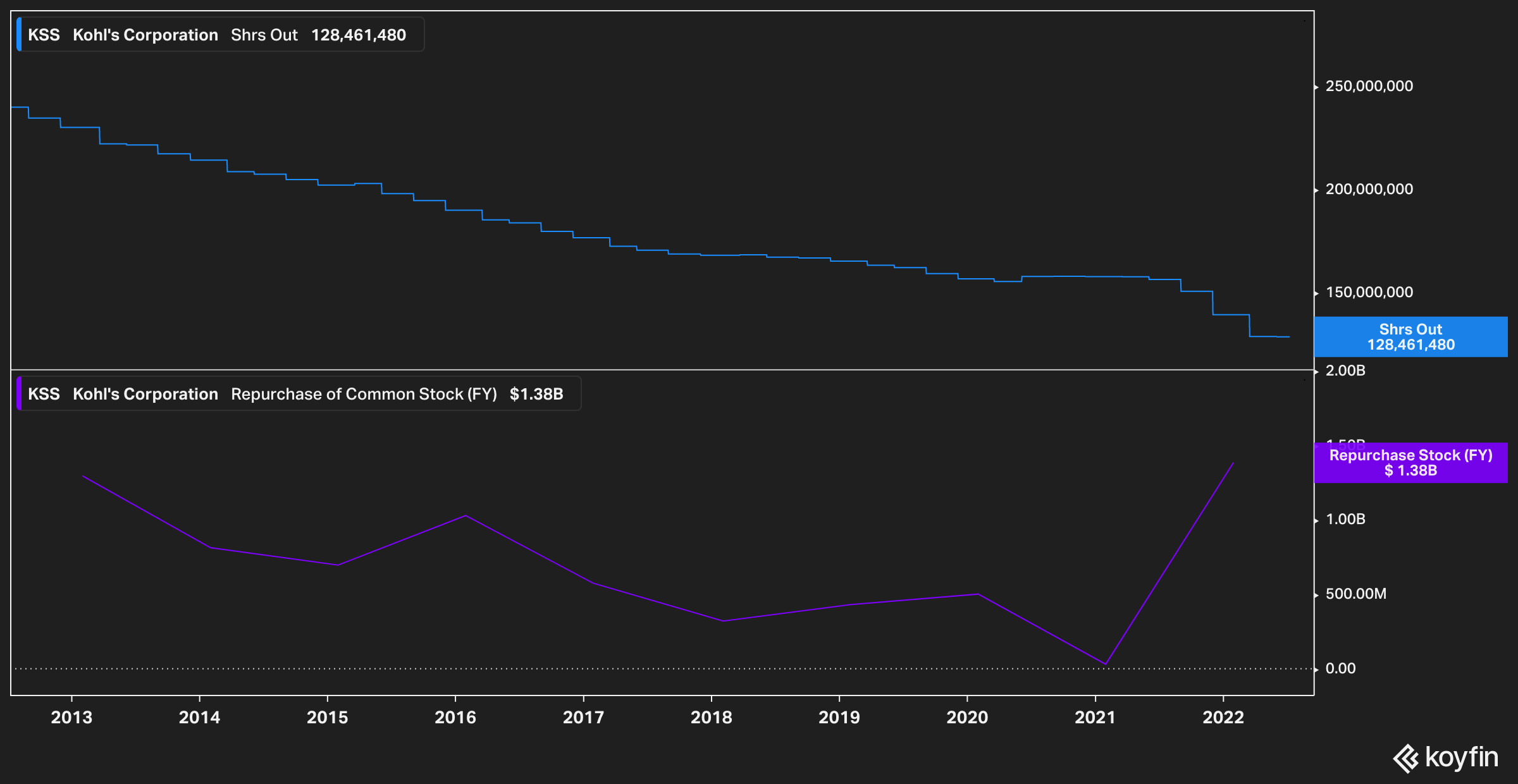

The company has historically been repurchasing shares aggressively, with share count almost halved over the past 10 years; resulting in increasing FCF per share (note that FCF has been positive every year since 2009). In addition, the company has authorized a $3 billion share repurchase program, with $500 million in accelerated share repurchases planned after Q2 results.

Unlike other retail concepts, the company has not been one of the main Covid beneficiaries, notably due to its relatively small exposure to home goods:

Shares are currently trading at only 5.2x EV/EBITDA and a 4.5x P/E based on the low point of management FY22 guidance. While guidance will likely be revised down, Kohl’s can likely earn around $5 to $6 of FCF per share on a normalized basis, which translates into a ~20% FCF yield at the current price. In addition, Kohl’s offers a ~7% dividend yield, largely covered by earnings.

All in all, it seems like Kohl’s shares are already pricing in a deep recession (or even worse). This is not exclusive to this name, as most retailers and consumer discretionary names are down significantly YTD. But the reality is that Kohl’s has valuable assets, has consistently been generating free cash flow in the past, is repurchasing shares aggressively, and is not one of the main Covid over-earners. Its strategy, particularly the Sephora partnership, makes sense and is gaining traction. If future results are not worse than what is currently feared, I expect Kohl’s shares to rerate substantially and would not rule out Franchise Group coming back to the negotiation table once financial conditions and the operating environment have stabilized.

Spirit Airlines (SAVE)

The Spirit / Frontier / JetBlue saga continues (link to my initial write-up and ), with Spirit delaying for a third time its special meeting related to the merger agreement with Frontier.

Since my latest update, the bidding war for Spirit Airlines has escalated, ultimately resulting in JetBlue offering an all-cash price of $33.50 per Spirit share, including the accelerated payment of $2.50 per share, as well as a ticking fee mechanism (monthly prepayment of $0.10 per share from January 2023 until the deal is consummated or terminated). As of this writing, the latest Frontier offer (1.9126 shares of Frontier per Spirit share, plus $4.13 in cash) values Spirit Airlines at $24.70, a 26% discount to JetBlue’s offer. With Spirit’s shares now trading at $24.90 (a small premium to Frontier’s offer, compared to an average discount of ~10% prior to JetBlue’s involvement), the market is pricing a non-zero chance for a bump to Frontier’s offer, or a preference for JetBlue’s bid.

The reason is obvious: the postponement of the special meeting means that Spirit does not have the votes required for the Frontier transaction. At the same time and before the first adjournment, approximately 12% of its shares were tendered into JetBlue’s $30 tender offer, which has been extended to July 29.

With the vote now scheduled for next Friday (July 15), JetBlue’s comments are growing increasingly positive:

We are encouraged by our discussions with Spirit and are hopeful they now recognize that Spirit shareholders have indicated their clear, overwhelming preference for an agreement with JetBlue. We strongly recommend that Spirit shareholders continue to let the Spirit Board know they want to receive the superior value JetBlue has proposed, by voting AGAINST the Frontier transaction.

The outcome of this battle for Spirit should unfold very soon, and it now seems that a transaction with Frontier on the current terms has very limited chances of happening.

Magnachip (MX)

More than a month and a half after the initial M&A chatter, a Korean media provided an update on the rumored deal with LX Group.

According to the article published yesterday, LX Group has completed its due diligence on Magnachip and could submit a final offer by the end of next week. However, it seems that their Private Equity partner won’t be participating in the offer.

Shares were down over the past couple of weeks given the lackluster outlook for semiconductors, but were up almost 10% of the news. It remains to be seen if LX Group will submit an appropriate bid for Magnachip, but I expect this situation to play out in the next couple of weeks and the risk-reward still seems compelling.