Twitter: done deal? And the Bally's opportunity.

Readers will know that the whole Musk/Twitter situation has been one of my main topics of interest in the past couple of weeks. After all, this Substack’s very first article was written on the potential Twitter buyout when shares were trading at $45.08, and I followed up on the situation when Musk announced his financing plan.

On Monday, Twitter announced that it was accepting Musk’s $54.20 offer (full disclosure: I sold all of my Twitter shares on Monday at $52 following the announcement). I was a little surprised that no other bidder showed interest in acquiring this asset, but I guess most of the obvious candidates had already enough on their plates, or were reluctant to get involved given the potential controversies around the platform, regulatory issues, or the restructuring required to make Twitter competitive.

I was still waiting to see the merger agreement to see if there was a go-shop provision, opening the door to other bidders and making a case for staying involved in the stock, but the answer is no:

Beginning on the date of the Merger Agreement, Twitter is subject to customary “no-shop” restrictions pursuant to which the Company may not, among other things: (1) solicit, initiate, knowingly encourage or knowingly facilitate any substantive discussion, offer or request that constitutes or would reasonably be expected to lead to a competing acquisition proposal; or (2) subject to certain exceptions, engage in negotiations or substantive discussions with, or furnish any material non-public information to, any person relating to a competing acquisition proposal or any inquiry or proposal that would reasonably be expected to lead to a competing acquisition proposal.

I think it’s pretty unlikely that someone will suddenly show up and outbid Musk. If anyone was interested, we would probably know by now. Given how fast the Board accepted Musk’s offer, I’m expecting Twitter’s Q1 2022 results to be weak, which would further reduce the likelihood of another bid. So in my eyes - Twitter is a done deal (although of course, a lot can still happen if the market and/or Tesla shares crash).

Which leads me to a similar opportunity…

Bally’s: another buyout candidate

Twitter was a situation where the implied odds of a buyout seemed too low. A similar situation in which I am currently involved in is Bally’s (ticker: BALY) - full disclosure: I am long shares of Bally’s.

Bally’s is a casino operator that, through a series of transactions, built a growing omni-channel presence in online sports betting and iGaming. It currently owns and manages 14 casinos across 10 states, a horse racetrack in Colorado and has access to OSB licenses in 17 states. It also owns Gamesys Group, an online gaming operator, and various other smaller assets.

On January 25, 2022, Standard General, a New York-based investment firm and Bally’s largest shareholder (with a 21% ownership of the company), delivered a non-binding proposal letter to Bally’s Board of Directors to acquire all of its outstanding shares for $38 per share. The connection doesn’t stop there - Soo Kim, Standard General’s Managing Partner and CIO, is also Bally’s Chairman.

A couple of days later, the Board of Directors formed a special committee of independent directors to evaluate the proposal, and retained financial and legal advisors on February 22nd.

The stock closed at $29.23 the day before the announcement, shot up around $36 after the offer was announced, and has since drifted lower to $27.53 at the time of writing.

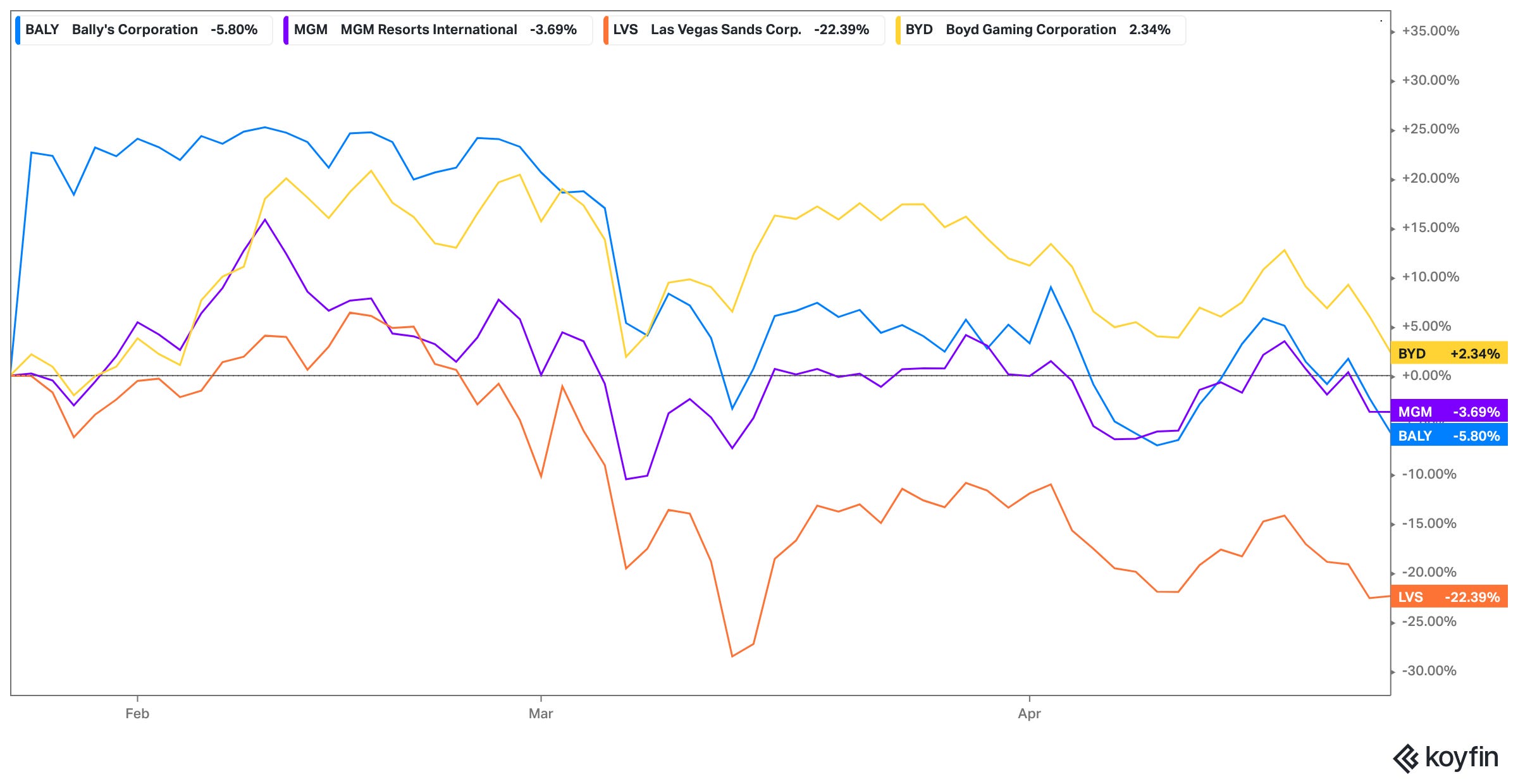

Comparing Bally’s share price action from the day before the offer to today, it has basically trended with its peer group (I’m using MGM, Las Vegas Sands, and Boyd Gaming):

Year-to-date, the picture is even worse, with Bally’s share significantly underperforming its peers:

That’s just share price though - what about valuation?

With 68m shares outstanding, the company currently has a market capitalization of $1.9B (using current share price of $27.5). Adding $3.4B of debt (excluding leases) gets us to an enterprise value of $5.3B.

Management has guided for $560-$580 million of EBITDA for 2022:

Using the mid-point of the guidance, Bally’s currently trades at 9.3x EV/EBITDA. However, note that this includes a $60m loss for the North America Interactive segment that is currently being scaled. Excluding this loss, we get to a 8.4x EV/EBITDA multiple for the core business, and the $38 offer would value it at 9.5x EV/EBITDA.

Is it fair? This name and its peer group have historically traded (before Covid) in a 9x to 13x EBITDA range:

At 9.5x EBITDA excluding the North America Interactive segment, the offer looks relatively fair relative to historical, pre-Covid multiples. However, Bally’s has significantly evolved since then, transitioning from an heterogeneous portfolio of land-based casinos to an omni-channel gaming company, which should deserve a higher multiple:

The special committee retained financial and legal advisors a little more than 2 months ago, so I would expect an update in the coming weeks and see 3 scenarios:

The offer is rejected: we end-up owning Bally’s at a 9.3x EV/EBITDA multiple (8.4x excluding North America Interactive). It does not look stretched relative to historical valuations and peers. Besides, Bally’s shares have not exactly outperformed peers since before the offer was announced, so it’s hard to see much downside (although shares would of course trade down on announcement).

The offer is accepted: assuming a 5% discount to take into account the timing and uncertainty around closing, shares would have ~30% upside (from the current price of $27.53 to $36, i.e. $38 minus our 5% discount).

Other bidders emerge: I wouldn’t exclude the emergence of competitive bidders, ultimately offering more than $38. After all, during a CNBC interview on the proposed takeover, Soo Kim mentioned that his bid essentially put the company in play.

Maybe I’m missing something, but odds seem to be skewed in our favor. There is a credible offer (although non-binding) on the table, with 30% upside to the current share price. This offer is relatively fair, but the company is now in play and I could definitely see competitive bidders emerging. And if no deal materializes, absolute and relative valuations are not stretched by any means so the downside could be relatively limited.

I’m looking forward to seeing how this situation unfolds.

open interest on the May 35 calls is fairly substantial and has been for over a month...somebody is looking for a meaningful event to happen before expiration..in my opinion the board should hold out for $48