Capricorn Energy (CNE.LN)

Money for nothing, Oil & Gas for free

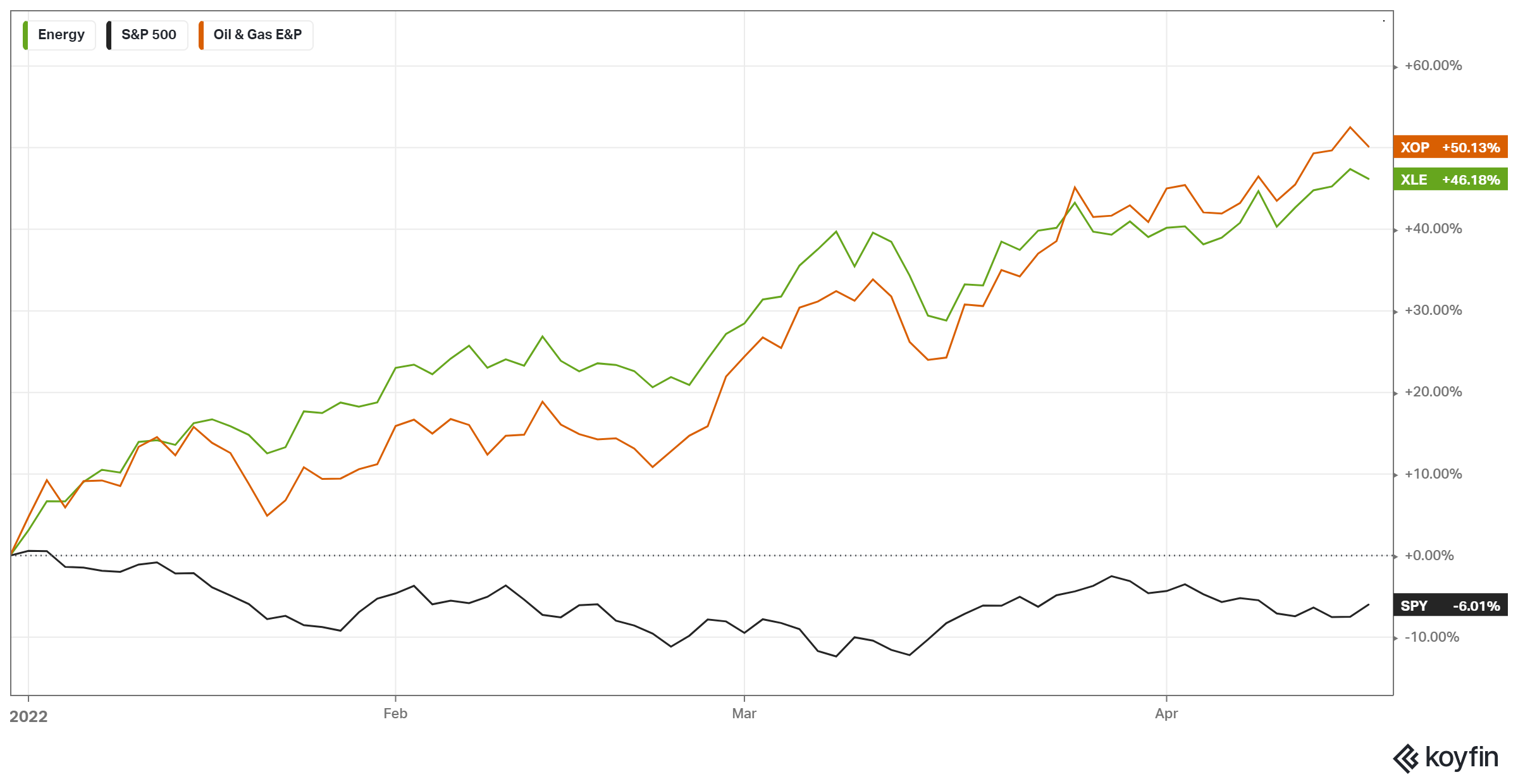

Energy is the hottest sector so far in 2022, thanks to skyrocketing oil and gas prices. The Energy sector ($XLE) and Oil & Gas E&P ($XOP) are up +46% and +50% YTD respectively, while the S&P index is down -6%.

While most companies in the sector have delivered solid returns, there are still major opportunities to be found, especially in special situations. One attractive name in this category right now is Capricorn Energy.

Company overview and recent events

Capricorn Energy (previously known as Cairn Energy) is a British oil and gas exploration and development company listed on the London Stock Exchange, with a long history of actively managing its portfolio of assets and returning cash to shareholders. After a long dispute with the Indian government regarding a retrospective capital gains tax on its Cairn India subsidiary, $1.7 billion were awarded to the company in December 2020, and, after initiating a number of enforcement proceedings in several jurisdictions during H1 2021, the long battle with the Government of India finally reached a resolution and a refund with net proceeds of $1.06 billion was received by the group in February 2022. This was of course a major development, as these proceeds represented nearly the entire market capitalization of the company. Yet, it seems that the market has simply been ignoring this event.

Following the receipt of the India award, Capricorn initiated a massive shareholder return program consisting of a tender offer for approximately $500m and an additional share buyback program of up to $200m.

The company ended 2021 with $133m of net cash on its balance sheet. Factoring in the receipt of the India tax refund, tender offer, the UK earn-out that the company is expected to receive in Q2 2022 (resulting from the sale of its UK production assets in 2021), I expect the company to end H1 2022 with $769m of net cash - ignoring for now any cash flow from operations as well as the impact of the ongoing buyback program.

Through its $500m tender offer, ~34% of shares outstanding were repurchased at an average price of 223 GBp, leading to a current fully diluted share count of 337 million (again, excluding any impact from the ongoing $200m buyback program):

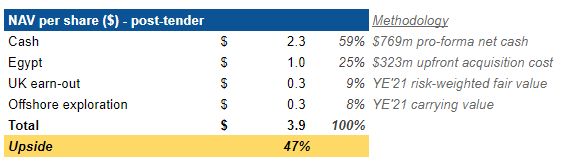

This leads us to an Enterprise Value for Capricorn Energy of $119 million, pro-forma of the upcoming UK earn-out payment:

What do we get for $119 million?

Capricorn’s assets

Capricorn Energy went through a complete portfolio overhaul over the past two years. It sold its Senegal and UK assets, and completed the acquisition of Shell’s Western Desert assets in Egypt.

Today, Capricorn Energy shareholders are getting exposure to a significant cash balance, as well as:

Production assets in Egypt, acquired from Shell in September 2021 for $323 million and with additional contingent consideration of up to a maximum of $140 million (all figures net to Capricorn, as it was acquired together with Cheiron).

Following this deal, Capricorn Energy owns working interest across four main concessions in Egypt, with production guidance of 37,000-40,000 boepd for 2022, and 2P reserves of 91 mmboe.

Capricorn has planned to spend $90-$110 million in new production and injection wells to optimize production, which should help exit 2022 with production rates well above 40,000 boepd.

While roughly two thirds of production is gas and sold domestically largely at a fixed price of $2.9/mcf, oil is expected to represent 35-40% of the production mix and is fully unhedged since December 31, 2021.

For reference, this asset generated on average $140m of cash flow from operations between 2017 and 2019, at lower oil prices and lower production levels than today (Brent averaged $58 over the period).

An additional UK earn-out consideration with a risk-weighted fair value of $113 million (a total of $189 minus the above-mentioned $76 to be received in Q2’22), resulting from the sale of Capricorn’s UK assets last year, and representing a share of future revenues generated by oil prices in excess of $52/barrel (uncapped), subject to minimum production levels being met.

Offshore exploration assets in Mexico, Suriname, Mauritania, UK, and Israel. Theses assets have a carrying value of $98 million as of December 31, 2021.

The largest asset is Egypt and is likely worth at least what Capricorn paid for it, given oil prices trajectory and its unhedged exposure. Maybe Capricorn overpaid for it, but (1) management has a significant experience in actively managing its portfolio, regularly buying and selling assets, and (2) as mentioned above, this asset generated $140m of CFFO per year over the 2017-2019 period. So by valuing it at $323m, we are essentially assuming it is worth 2.3x its average CFFO over a period were oil prices were significantly lower than today, and when production was not optimized due to under-investments in CAPEX under Shell’s ownership.

The UK earn-out consideration and offshore exploration assets are more complex to value, but if we trust Capricorn’s book then these are worth an additional ~200 million.

All in all, I think we can be relatively confident that Capricorn’s assets are worth north of $500 million.

Valuation and upside

At the current share price of 201.6 GBp or 2.6 USD (as of close on 04/20/2022), we are basically paying for the cash and UK earn-out and getting the production and exploration assets for free:

87% of the share price (59% of NAV) is covered by cash, and with ongoing buybacks, the downside appears very limited. Meanwhile, shares trade at a 32% discount to my conservative estimate of NAV.

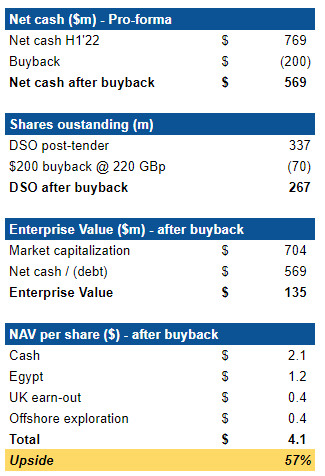

Note that this is before considering the impact of the current buyback program. Assuming they manage to complete the $200m buyback at an average share price of 220 GBp, the share count would be reduced by another 70 million, leading to a $4.1 NAV/share (57% upside to current share price):

And remember I just use the acquisition cost on Egypt, an asset that generated ~$140m of CFFO in 2017-2019 at $58 Brent prices. What if through a combination of operational improvements and higher oil prices we get to $200m of CFFO valued at 2.5x CFFO? That’s $500m for this asset and an additional $0.5 to NAV, leading to 75% upside.

But of course, most of the value is in cash, meaning most of the value creation still lies in management’s hands. What are the options here?

James Smith (Capricorn Energy’s CFO) mentioned during the Q4 2021 earnings call that acquisitions were a priority, but additional returns to shareholders were not out of the question:

As we talked about the balance sheet, following the India tax refund and the US$500 million tender offer, we'd still retain a significant funding firepower to further build out our cash flow base through acquisition, focused on opportunities with similar characteristics to those I've just listed regarding Egypt. And then ultimately, we continue to see returning cash to shareholders as a key differentiator of Capricorn. Clearly, we're in the midst of a very significant capital return right now, but as we continue to build the business from here, we'll continue to ensure that fiscal discipline of investing for sustainable growth through the cycle, but also continuing to build opportunities to return further value to shareholders.

I’m not going to run through the additional buybacks/special dividends scenarios, but the math can get crazy pretty quickly here and it’s not impossible to envision over 100% upside. Maybe management will light all this money on fire, but I think it’s pretty unlikely given their experience in actively managing their asset portfolio and the long history of returning cash to shareholders through special dividends and share repurchases.

Conclusion

Capricorn Energy is a special situation in the Oil & Gas sector. It might not have the most torque to higher oil prices, but the downside appears very limited given the significant cash position and ongoing buybacks.

In 12 months, investors will have a clearer view of the cash flow potential of Egypt. Cash will likely have been put to use (either through acquisitions, additional shareholder returns, or a mix of both). And Capricorn Energy will likely be valued based on its operating assets. In the meantime, management has several levers to pull to create shareholder value, and history shows that they can be trusted to prioritize shareholders returns over empire building, resulting in what I believe is a very compelling and asymmetric opportunity.

What is the current situation regarding extremely undervalued takeover proposal?